The world of finance is on the verge of changes. Having a significant impact on other business sectors, the stock exchange serves as an important mechanism and a key factor for companies to raise capital. Since assets on the US Stock Exchange will increase to $ 40 trillion in 2023, which is 1.5 times greater than the country's GDP, it is a significant part of the general economy, emphasizing its important position as a reference point for the American economic landscape.

Two outstanding scientists from South Dakota State University – Kaiqun Fu, an experienced professor's assistant at the Faculty of Electrical Engineering and Computer Science, together with a graduate of student researcher Yanxiao Bai, presented a very interesting model of artificial intelligence called “Alerta -Net”. This deep neural network is gaining an exceptional advantage by combining macroeconomic indicators, search engines and social media context. Raises the question: Can AI tools be the key to predicting stock movements and stock exchange variability? Let's take a closer look at these innovative research and their potential impact on the financial landscape.

Their research focuses on Blue Chip actions, which reflect the wider dynamics of the stock market. Blue Chip shares are actions broadcast by justified, well -established companies with impeccable reputation.

Scientists chose 41 Blue Chip shares from 10 sectors in accordance with the global standard of industry classification (GICS) to examine the financial market. Each of these actions is considered an investment prospect of both Moody's and S&P. Considering the known difficulties in accurate forecasting of share prices, scientists decided to use Blue Chip shares to predict the upcoming movements of share prices and trends of variability.

The two main methodologies prevail in stock market research: technical and fundamental analysis. Technical analysis uses previous share prices to predict future trends. However, his great reaction to historical data can sometimes skip sudden market changes due to unexpected events. Assuming a uniform rational market behavior, this methodology can sometimes create a random Echo chamber, causing that trade signals are insulated from a true economic context.

On the other hand, fundamental analysis integrates both price features and external information, including data from social media and search engines. This approach shows better accuracy of closing the S&P 500 index during data integration on Twitter with its model. Although these data sources often reflect not only the financial market, but also important economic indicators, the dominant research in fundamental analysis emphasizes the financial market, neglecting the symbiotic relationship between the general economy and the stock market. In addition, existing models focus mainly on predicting trend changes, often neglecting the importance of the scale of these changes. But in the area of spare behavior, the scale of these changes is significant.

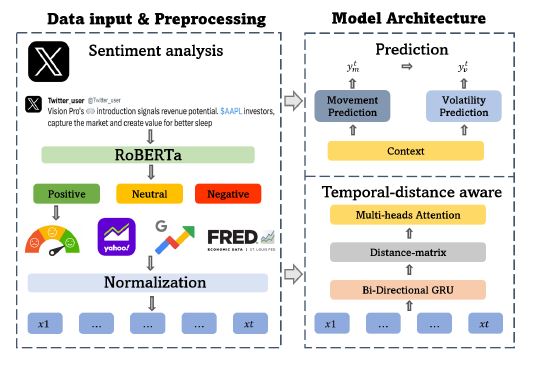

In their article, published On the Preprint Arxiv server, scientists offer a new model that connects both approaches. Alerta-Net-Nouwa in times of repetitive neural networks. The proposed framework allows you to combine data from social networks, macroeconomic indicators and search engines to predict the movements of stock prices and variability.

Let's consider the general architecture of Alerta-Net. A layer of data entering and pre -processing transforms both time and text information into dense vectors. Then the time layer of distance awareness has a repetitive representation that identifies hidden dependencies in current spare data based on previous information. Then the context of the distance matrix integrates these historical dependencies with the sequence of features. And finally, the prognosis layer generates corrected time for spare traffic and variability forecasts for the next time, thus ensuring a complete and coherent system forecasting system.

The Alerta-Net architecture has been designed to predict movement and variability on the day of the data entry phase and initial processing separates textual information from Twitter and transforms it into sentiments. AERTA-NET then uses these sentiment results along with other functions to make forecasts based on time distance.

To confirm the effectiveness of the proposed model, experiments and comparisons were carried out Data set. The data set provides sentiments for 41 Blue Chip stocks and combines three main components: price data, data on Twitter moods and macroeconomic data.

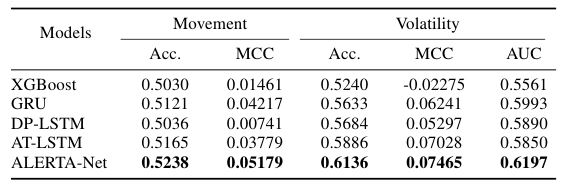

Alerta-NET performance has been evaluated compared to DP-LSTM, a well-known spare traffic forecasting network based on financial data. Other tests used in the study include an extreme increase in gradient, LSTM based on comments and GRU. The results are defined in terms of accuracy and Matthews correlation coefficient. Considering that data points covering share prices by more than 5% constituted only a small part of the data set, it was decided to use the area under the ROC (AUC) curve as a measure of performance to achieve a more reliable and realistic forecast. The results are shown in the table below.

Thanks to Alerta-NET, it becomes possible not only to predict share price movements, but also effectively obtain information about the variability of the stock market. This allows you to predict all unusual fluctuations on the stock exchange in the future.

Alerta-Net proved in the recognition of dynamic, temporary distances of the distance embedded in various hidden states. Using share prices on the same day, the model significantly increases its accuracy in predicting stock exchange variability.

In general, Alerta-Net, deep generative architecture of the neural network, showed the effectiveness of combining data on search engines, macroeconomic indicators and social media data to try to forecast movements and reserve variability. In future research, scientists plan to improve accuracy by integration of many sources of text and sound, including combinations of profits and financial statements.

{kind=link}